In the low interest rate environment of the past several years, master limited partnerships (MLPs) became quite popular and were promoted by brokers as investments that would earn a strong yield-based return while retaining the potential for capital appreciation. MLP IPOs raised more than $100 billion since the global financial crisis. Recently, however, the current values of many MLPs have plummeted (many by more than 50%) and the high yields have come to an end as falling energy prices and doubt about the future of the industry have caused the partnerships to suspend or decrease their dividends. This has caught many investors—particularly those who replaced their relatively safe fixed-income investments with MLPs—by surprise as brokers tended to promote the supposed benefits of MLPs (including by referencing the high returns of the past) without adequate disclosure of the substantial risks associated with MLPs (such as their stock-like characteristics and high concentration in the energy industry).

What is a Master Limited Partnership?

A master limited partnership, which is sometimes referred to as a publicly traded partnership, is a limited partnership that is publicly traded on an exchange. It seeks to combine the tax benefits of a limited partnership with the liquidity of a publicly traded security. As a partnership, MLPs do not pay entity-level income taxes and instead pass all income, gains, deductions, losses, and credits through to investors. Because they are publicly traded on an exchange, MLPs are available to any investor with a brokerage account and can be bought and sold throughout the trading day.

Today, MLPs are primarily concentrated in the energy sector. MLPs first came about in the early 1980s (Apache Corporation became the first company to structure as an MLP in 1981). At the time, there were no real restrictions on the types of businesses that could operate as MLPs. As a result, companies all over the spectrum began to form as MLPs. To prevent the loss of tax revenues, Congress passed legislation designed to restrict the types of companies that could form MLPs. Now, to qualify as an MLP under the Internal Revenue Code, a partnership must generate at least 90 percent of its income from “qualifying” sources. These “qualifying” sources generally include income related to the energy industry, such as those related to the exploration, production, processing, and transportation of oil, natural gas, and coal.

Unlike a real estate investment trust (REIT), MLPs do not have a statutory requirement to distribute a certain amount of its income to investors. Because MLPs are typically valued based on a multiple of their cash flow, they tend to distribute all available cash (cash over and above that required for operations and debt service) to investors. This, combined with absence of corporate taxes, has historically created the high-yield for investors.

MLPs generally have two categories of ownership: the general partner and the limited partners. The general partner’s ownership interest is typically held by a holding company owned by a major energy company. The limited partners’ ownership interest is held by the investors and traded on an exchange. The general partner, although it generally owns a very small portion of the MLP compared to the combined value of the limited partners, controls and manages the MLP.

Investing in MLPs

The number of MLPs has more than tripled over the last ten years as the low interest rate environment has driven investor demand, and MLPs have raised more than $100 billion in IPOs since 2008. According to Alerian (an independent provider of MLP and energy infrastructure market intelligence), as of December 31, 2015, there were 121 different MLPs with a total market capitalization of about $300 billion. Just a year earlier, MLPs had a market capitalization of over $450 billion.

The top 10 MLPs (in terms of market capitalization) include Enterprise Products Partners, LP (EPD); Energy Transfer Partners, LP (ETP); Magellan Midstream Partners, LP (MMP); MPLX, LP (MPLX); Plains All American Pipeline, LP (PAA); Buckeye Partners, LP (BPL); Williams Partners, LP (WPZ); ONEOK Partners, LP (OKS); Enbridge Energy Partners, LP (EEP); Sunoco Logistics Partners, LP (SXL).

In addition to buying individual MLPs, investors may invest in MLPs through a variety of funds that invest in MLPs. Investors may gain MLP investment exposure through exchange-traded funds (ETFs), mutual funds (open-end funds), closed end funds, and structured notes. Although these products are available to retail investors, many are not easily understood, such as structured notes that are issued by and are the obligation of a financial institution, but have payoffs that are linked to the returns of an MLP index.

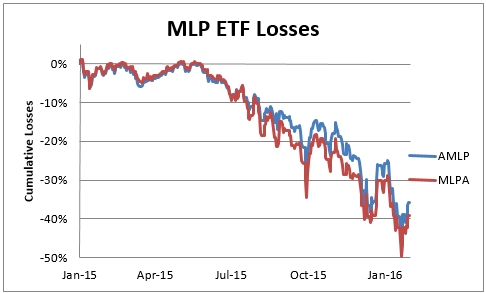

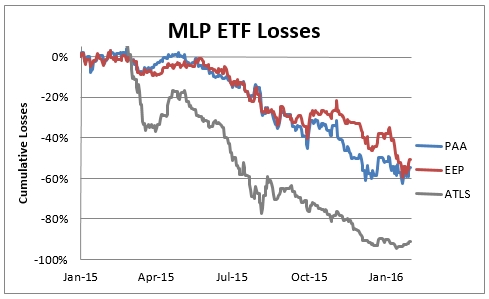

As global energy prices have declined over the past year, MLPs have suffered staggering losses. The Alerian MLP Index, which tracks the performance of the 50 largest MLPs, declined by 32.6% in 2015. Not surprisingly, the returns of ETFs investing in MLPs have declined precipitously: the Alerian MLP ETF (AMLP) lost 35.9% from January 1, 2015 to January 31, 2016. Similarly, the Global X MLP ETF (MLPA) lost 39.2% over that timeframe. Smaller MLPs suffered even greater losses: Atlas Energy (ATLS) lost a staggering 91.3%, Plains All American Pipeline (PAA) lost 54.4%, and Enbridge Energy Partners LP (EEP) lost 50.8%. The following charts illustrate the dramatic losses suffered by MLP investors since 2015.

What are the risks of MLPs?

MLPs carry two primary risks: stock-like characteristics and high concentration in one industry (energy). First, they involve stock-like volatility and risk. While they are promoted as fixed-income investments similar to bonds, an investment in MLPs represents an equity stake in the company. Investors are subject to price movement of the MLPs and only share in profits after payment of debt (such as bond interest payments). Investors replacing traditional fixed income investments (such as bonds) with MLPs may have unintentionally increased their portfolio’s volatility and risk profile. Second, because of the legislation passed in the 1980s, MLPs are typically restricted to the energy sector. Thus, MLPs have little diversification beyond different elements of the energy sector, and they will tend to rise and fall along with the price and volume of energy products being produced and sold. Another less commonly discussed risk is lack of management control. In a traditional corporation, the management is controlled, at least indirectly, by the voting power of the shareholders. In an MLP, however, management is vested in the general partner. Limited partners, despite the amount of interest in the MLP they may own, have very limited control over the management and operations of the MLP.

Many investors held portfolios that were overly concentrated to these products. Even a diversified portfolio of MLPs remains heavily concentrated in exposure to the energy sector. Additionally, structured notes contain counter-party risk and frequently use derivatives to embed leverage.

Here is a current list of MLPs and funds investing in MLPs by ticker symbol and name. If you have invested in these products and suffered losses, we would like to speak with you.

| Ticker | Name |

| AHGP | Alliance Holdings GP LP |

| ARLP | Alliance Resource Partners LP |

| ALDW | Alon USA Partners LP |

| AMID | American Midstream Partners LP |

| APU | AmeriGas Partners LP |

| AM | Antero Midstream Partners LP |

| ARCX | Arc Logistics Partners LP |

| APLP | Archrock Partners LP |

| ATLS | Atlas Energy Group LLC |

| ARP | Atlas Resource Partners LP |

| AZUR | Azure Midstream Partners LP |

| BSM | Black Stone Minerals LP |

| BKEP | Blueknight Energy Partners LP |

| BWP | Boardwalk Pipeline Partners LP |

| BBEP | BreitBurn Energy Partners LP |

| BPL | Buckeye Partners LP |

| CLMT | Calumet Specialty Products Partners LP |

| CPLP | Capital Product Partners LP |

| CQP | Cheniere Energy Partners LP |

| CNXC | CNX Coal Resources LP |

| CPPL | Columbia Pipeline Partners LP |

| CNNX | CONE Midstream Partners LP |

| CEQP | Crestwood Equity Partners LP |

| CAPL | CrossAmerica Partners LP |

| CCLP | CSI Compressco LP |

| UAN | CVR Partners LP |

| CVRR | CVR Refining LP |

| CELP | Cypress Energy Partners LP |

| DPM | DCP Midstream Partners LP |

| DKL | Delek Logistics Partners LP |

| DM | Dominion Midstream Partners LP |

| DMLP | Dorchester Minerals LP |

| DLNG | Dynagas LNG Partners LP |

| EMES | Emerge Energy Services LP |

| ENBL | Enable Midstream Partners LP |

| EEP | Enbridge Energy Partners LP |

| ETE | Energy Transfer Equity LP |

| ETP | Energy Transfer Partners LP |

| ENLK | EnLink Midstream Partners LP |

| EPD | Enterprise Products Partners LP |

| EQGP | EQT GP Holdings LP |

| EQM | EQT Midstream Partners LP |

| EVEP | EV Energy Partners LP |

| FGP | Ferrellgas Partners LP |

| FELP | Foresight Energy LP |

| GLOP | GasLog Partners LP |

| GEL | Genesis Energy LP |

| GLP | Global Partners LP |

| GMLP | Golar LNG Partners LP |

| GPP | Green Plains Partners LP |

| HCLP | Hi-Crush Partners LP |

| HMLP | Hoegh LNG Partners LP |

| HEP | Holly Energy Partners LP |

| JPEP | JP Energy Partners LP |

| KMI | Kinder Morgan |

| KNOP | KNOT Offshore Partners LP |

| LGCY | Legacy Reserves LP |

| LINE | Linn Energy LLC |

| MMP | Magellan Midstream Partners LP |

| MMLP | Martin Midstream Partners LP |

| MEMP | Memorial Production Partners LP |

| MEP | Midcoast Energy Partners LP |

| MCEP | Mid-Con Energy Partners LP |

| MPLX | MPLX LP |

| NRP | Natural Resource Partners LP |

| NAP | Navios Maritime Midstream Partners LP |

| NSLP | New Source Energy Partners LP |

| NGL | NGL Energy Partners LP |

| NKA | Niska Gas Storage Partners LLC |

| NTI | Northern Tier Energy LP |

| NS | NuStar Energy LP |

| NSH | NuStar GP Holdings LLC |

| OCIP | OCI Partners LP |

| OKS | ONEOK Partners LP |

| PBFX | PBF Logistics LP |

| PTXP | PennTex Midstream Partners LP |

| PSXP | Phillips 66 Partners LP |

| PAA | Plains All American Pipeline LP |

| RNF | Rentech Nitrogen Partners LP |

| RHNO | Rhino Resource Partners LP |

| RMP | Rice Midstream Partners LP |

| RRMS | Rose Rock Midstream LP |

| SPP | Sanchez Production Partners LP |

| SDLP | Seadrill Partners LLC |

| SHLX | Shell Midstream Partners LP |

| SXE | Southcross Energy Partners LP |

| SEP | Spectra Energy Partners LP |

| SRLP | Sprague Resources LP |

| SGU | Star Gas Partners LP |

| SPH | Suburban Propane Partners LP |

| SMLP | Summit Midstream Partners LP |

| SXCP | SunCoke Energy Partners LP |

| SXL | Sunoco Logistics Partners LP |

| SUN | Sunoco LP |

| TEP | Tallgrass Energy Partners LP |

| NGLS | Targa Resources Partners LP |

| TCP | TC PipeLines LP |

| TGP | Teekay LNG Partners LP |

| TOO | Teekay Offshore Partners LP |

| TNH | Terra Nitrogen Co LP |

| TLLP | Tesoro Logistics LP |

| TLP | TransMontaigne Partners LP |

| RIGP | Transocean Partners LLC |

| USAC | USA Compression Partners LP |

| USDP | USD Partners LP |

| VLP | Valero Energy Partners LP |

| VNR | Vanguard Natural Resources LLC |

| VNOM | Viper Energy Partners LP |

| VTTI | VTTI Energy Partners LP |

| WGP | Western Gas Equity Partners LP |

| WES | Western Gas Partners LP |

| WNRL | Western Refining Logistics LP |

| WLKP | Westlake Chemical Partners LP |

| WMLP | Westmoreland Resource Partners LP |

| WPZ | Williams Partners LP |

| WPT | World Point Terminals LP |

|

Exchange-Traded Funds |

|

| AMLP | Alerian MLP ETF |

| AMJ | JP Morgan Alerian MLP Index ETN |

| MLPI | UBS ETRACS Alerian MLP Infrastructure Index |

| MLPN | Credit Suise X-Links Cushing MLP Infrastructure ETNs |

| AMU | ETRACS Alerian MLP Index ETN |

| IMLP | iPath S&P MLP ETN |

| MLPA | Global X MLP ETF |

| ATMP | Barclays ETN+ Select MLP ETN |

| MLPL | UBS ETRACS 2xLeveraged Long Alerian MLP Infrastructure Index |

| MLPX | Global X MLP & Energy Infrastructure ETF |

| EMPL | First Trust North American Energy Infrastructure Fund |

| YMLP | Yorkville High Income MLP ETF |

| MLPO | S&P MLP ETN |

| MLPY | Morgan Stanley Cushing MLP High Income ETN |

| ZMLP | Direxion Zacks MLP High Income Shares |

| MLPB | ETRACS Alerian MLP Infrastructure ETN B |

| YMLI | Yorkville High Income Infrastructure MLP ETF |

| AMUB | ETRACS Alerian MLP Index ETN Series B |

| AMZA | InfraCap MLP ETF |

| TPYP | Tortoise North American Pipeline Fund |

| MLPG | UBS ETRACS Alerian Natural Gas MLP Index |

| YGRO | RBC Yorkville MLP Distribution Growth Leaders Liquid Index ETN |

| MLPV | ETRACS 2xMonthly Leveraged S&P MLP Index ETN |

| MLPW | UBS ETRACS Wells Fargo MLP Index |

| MLPS | ETRACS 1xMonthly Short Alerian MLP Infrastructure Total Return ETN |

| MLPJ | Junior MLP ETF |

|

Open End Funds |

|

| TORTX | Tortoise MLP and Pipeline |

| MLOAX | Cohen & Steers MLP & Energy Opportunity Fund |

| TMLAX | Transamerica MLP & Energy Income |

| LCPAX | Clearbridge Energy MLP & Infrastructure Fund |

| MLPFX | Oppenheimer Steelpath MLP Select 40 Fund |

| INFRX | Advisory Research MLP and Energy Income |

| PRPAX | Prudential Jennison MLP Fund |

| MLPPX | MLP and Energy Infrastructure Income Fund |

| SMAPX | Salient MLP and Energy Infrastructure Fund II |

| GLPAX | Goldman Sachs MLP Energy Infrastructure Fund |

| EGLAX | Eagle MLP Strategy Fund |

| ILPAX | Invesco MLP Fund |

| MLXAX | Catalyst MLP & Infrastructure Fund |

| MLPAX | Oppenheimer Steelpath MLP Alpha Fund |

| CCCAX | Center Coast MLP Focus |

| BPMIX | BP Capital TwinLine MLP Fund |

| AMLPX | Maingate MLP |

| MLPDX | Oppenheimer Steelpath MLP Income Fund |

| CSHAX | Cushing MLP Premier Benefits Fund |

| MLPLX | Oppenheimer Steelpath MLP Alpha Plus Fund |

| HEFAX | Highland Energy MLP Fund |

| VMLPX | MAI Energy Infrastructure and MLP Fund |

|

Closed End Funds |

|

| FIF | First Trust Energy Infrastructure |

| FPL | First Trust New Opportunities MLP and Energy Fund |

| GER | Goldman Sachs MLP and Energy Renaissance Fund |

| FEN | First Trust Energy Income and Growth |

| CEN | Center Coast MLP & Infrastructure Fund |

| TPZ | Tortoise Power and Energy Infrastructure |

| KYN | Kayne Anderson MLP Investment Company |

| TTP | Tortoise Pipeline and Energy |

| KYE | Kayne Anderson Energy Total Return Fund |

| NML | Neuberger Berman MLP Income Fund |

| SRV | Cushing MLP Total Return Fund |

| GMZ | Goldman Sachs MLP Income Opportunities Fund |

| SMM | Salient Midstream and MLP Fund |

| TYG | Tortoise Energy Infrastructure Corp |

| NTG | Tortoise MLP Fund |

| FMO | Fiduciary/Claymore MLP Opportunity |

| JMPL | Nuveen All Cap Energy MLP Opportunity Fund |

| JMF | Nuveen MLP Total Return Fund |

| SRF | Cushing Royalty and Income Fund |

| KED | Kayne Anderson Energy Development Company |

| CEM | ClearBridge Energy MLP Fund |

| KMF | Kayne Anderson Midstream/Energy |

| CBA | Clearbridge American Energy MLP Fund |

| EMO | ClearBridge Energy MLP Opportunity Fund |

| DSE | Duff & Phelps Select Energy MLP Fund |

| CTR | ClearBridge Energy MLP Total Return Fund |

| MIE | Cohen & Steers MLP Income and Energy Opportunity Fund |

Fishman Haygood represents investors who have suffered investment losses in claims against their brokers or financial advisors. Our experienced attorneys have brought securities fraud cases in state and federal courts across the nation, as well as in FINRA arbitration. We work to help investors recoup their losses.

Of course, all cases are different. For that reason, we analyze each client’s matter individually and provide our personalized evaluation only after considering all of the facts and circumstances of all possible claims. If you or someone you know is the victim of securities fraud, please contact a Fishman Haygood lawyer today.